Samsung Electronics and LG Electronics are making their most aggressive moves yet into the European heat pump market, deploying billion-dollar acquisitions and next-generation refrigerant platforms as binding EU decarbonization policy drives a structural shift away from fossil-fuel heating in residential and commercial buildings.

Background

European heat pump sales dropped 22 percent in 2024, falling for a second consecutive year after a boom triggered by the 2022 energy crisis, according to the European Heat Pump Association.[1] The downturn did not deter the two Korean manufacturers. Instead, both used the market correction to build strategic European footholds through targeted acquisitions.

Heat pump sales in 2025 grew by 10.3% across 16 European countries on average, with around 2.62 million residential heat pumps sold, preliminary data from the European Heat Pump Association shows, bringing the total installed base in Europe to approximately 28 million units. The recovery reflects improved policy stability across multiple member states. Governments that have stabilized subsidy schemes and acted on costs - for example, by reducing taxes on electricity bills - have made heat pumps highly competitive with fossil-fuel boilers.

On the regulatory side, the EU's revised Energy Performance of Buildings Directive requires all new public buildings to meet zero-emission standards from 2028.[2] The phaseout of financial incentives for stand-alone fossil-fuel boilers as of January 2025 provides a strong policy push toward non-fossil heating appliances.

Details

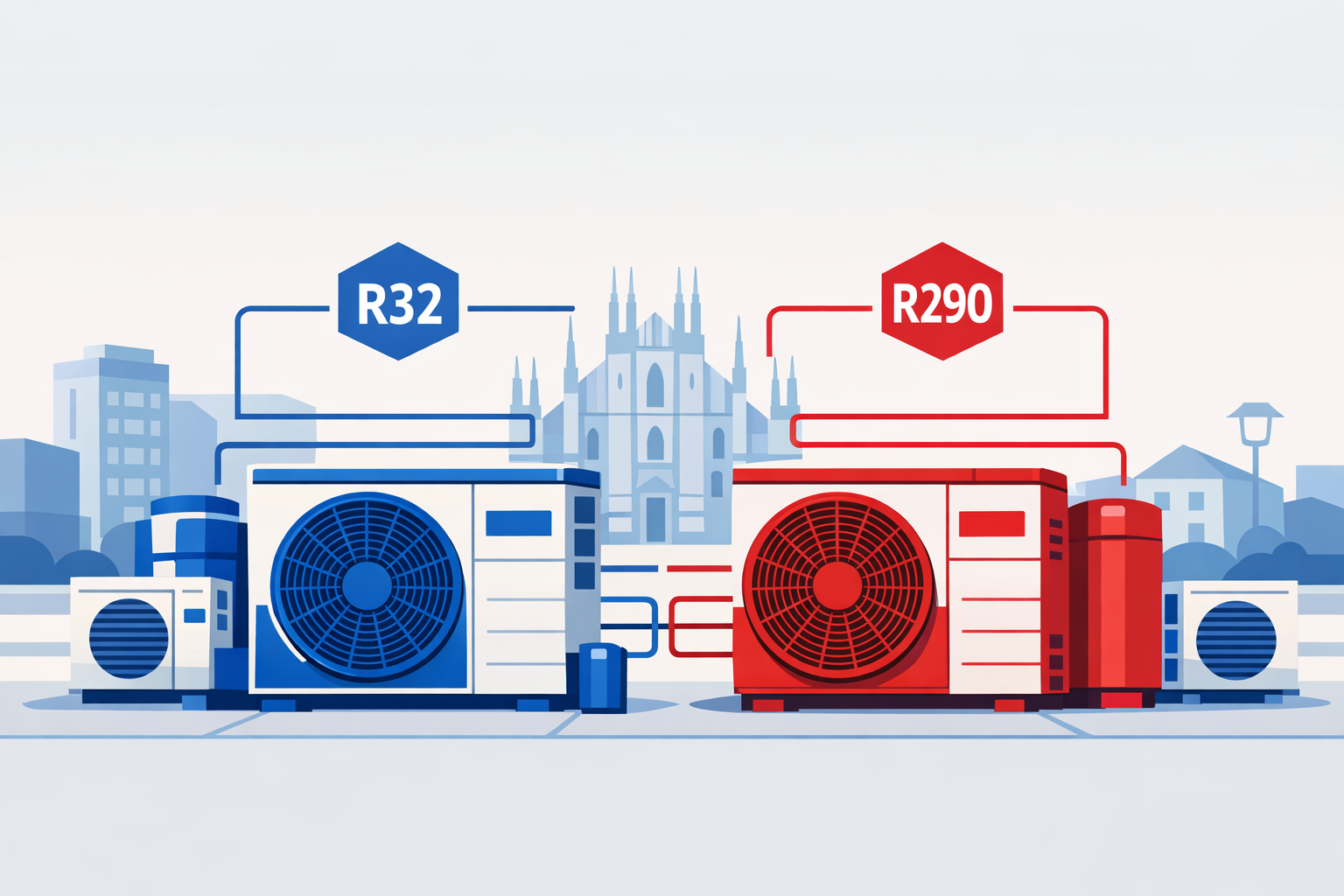

Samsung Electronics and LG Electronics both exhibited at Europe's largest HVAC trade fair, Mostra Convegno Expocomfort (MCE) 2026 in Milan, showcasing residential, commercial, and industrial HVAC solutions in a direct contest for European market share.

Samsung's appearance at MCE marked its first joint exhibition with Fläktgroup, the German climate-control specialist it acquired in November for 1.5 billion euros ($1.8 billion).[3] LG showcased systems integrating technology from OSO, a Norwegian hot-water solutions firm it acquired last July for an undisclosed sum.[4]

The two companies are pursuing differentiated refrigerant strategies ahead of Europe's F-Gas phase-down rules. Samsung's new EHS All-in-One system, launched in Europe this year, uses R32, a refrigerant whose global warming potential is roughly 68 percent lower than the industry-standard R410A.[5] LG went further with its Therma V R290 Monobloc, which runs on propane-based R290 - a natural refrigerant with a near-zero climate footprint. LG also debuted a compact combi unit with a built-in water tank designed for space-constrained European apartments.

On efficiency, Samsung's Eco Heating System heat pump recorded a coefficient of performance (COP) of 4.90, meaning it produces approximately 4.9 times more heating energy than a standard fossil-fuel boiler under identical conditions. LG's heat pump claims heating efficiency about 4.9 times greater and a carbon dioxide reduction effect of 68% compared to conventional boilers.

Both manufacturers have begun securing project-level contracts to validate their distribution reach. Samsung has won a contract to supply heat pump systems for a large residential redevelopment in Cornwall, England, while LG is providing units for housing projects in Eindhoven and Ridderkerk in the Netherlands. LG has sold heat pumps to more than 100,000 households in five southern European countries, including France and Spain.

LG's divisional leadership has publicly committed to further regional investment. "We will accelerate our push into the European heat pump market with integrated heating, cooling, and hot water system solutions," said Lee Jae-sung, head of LG Electronics' ES Business Division.

Installer Shortage Remains a Structural Bottleneck

Persistent workforce constraints represent the most significant demand-side risk to both manufacturers' European rollout plans. To scale heat pump deployment and meet 2030 climate goals, an estimated 750,000 more installers are needed, and at least 50% of existing installers will have to be reskilled to work with heat pumps, according to the European Commission.

Eurostat reports that only 30% of HVAC technicians in Europe are trained to work with heat pump technologies, leaving a substantial skills gap. The specialized knowledge required for proper system sizing, refrigerant handling, and hydraulic integration means inadequate installations are a growing concern that could erode consumer confidence. The shift to low-GWP refrigerants such as R290 introduces additional retraining requirements, as propane-based systems demand certified flammable-refrigerant handling competencies that most existing heating engineers do not hold.

The European heat pump market was valued at an estimated USD 14.2 billion in 2024 and is expected to reach USD 16.8 billion in 2025, with projections pointing to USD 82.6 billion by 2034 at a CAGR of 19.3%. For HVAC professionals, distributors, and system designers, the intensifying Samsung-LG rivalry signals both broader product availability and an accelerating need for certified upskilling - particularly around next-generation refrigerants, hydraulic integration, and smart system commissioning. For further context on low-GWP refrigerant transitions affecting SHK procurement, see earlier coverage in Global Refrigerant Market in Flux and the broader market outlook in Global HVAC Market Poised for Surge by 2035.

Outlook

Twelve of the 16 countries tracked by EHPA installed more heat pumps in 2025 than in 2024, largely because governments stabilized subsidy schemes and acted to reduce electricity costs. With EU building regulations tightening through 2028 and national boiler-ban timelines hardening in key markets including the Netherlands and the UK, the structural demand trajectory is unlikely to reverse. The critical test for Samsung and LG will be whether their European service and training networks can scale alongside product rollouts - and whether the broader installer workforce can keep pace with accelerating policy-driven demand.