Data center operators across North America and Europe are accelerating adoption of hybrid air-liquid cooling systems as converging regulatory deadlines and AI-driven thermal loads force a structural shift away from legacy high-GWP refrigerants. The transition is reshaping procurement strategies, facility design standards, and workforce requirements at mission-critical facilities of all scales.

Background

A global regulatory shift is forcing the cooling industry to rethink its dependence on high-GWP refrigerants. These substances have powered decades of efficiency and reliability in traditional HVAC systems but now face tightening environmental policy, with compliance timelines shorter than most data center operators are accustomed to.[1]

In the United States, the EPA's Technology Transitions Rule, enacted under the 2020 American Innovation and Manufacturing (AIM) Act, restricts new air conditioning and heat pump equipment to refrigerants with a GWP below 700, effective January 1, 2025, according to ACHR News. All new data center cooling equipment must comply with the GWP-below-700 threshold by January 1, 2027. California, Washington, and New York have established even earlier compliance deadlines, with California requiring a GWP below 750 in new equipment as of January 1, 2025, according to ACHR News. On the other side of the Atlantic, EU Regulation 2024/573 requires liquid chillers above 12 kW to use refrigerants with a GWP below 750 from January 1, 2027, with further restrictions tightening to GWP below 150 for many AC packaged units from the same date, according to Vertiv.

HFCs such as R-134a and R-410A, mainstays in many data center cooling systems, carry global warming potentials thousands of times greater than CO₂. R-410A carries a GWP of 2,088, meaning its climate impact is 2,088 times greater than carbon dioxide, according to Vertiv. For a data center operating continuously, even minor leaks of high-GWP refrigerants accumulate into significant emissions over time.

Details

Cooling systems in data centers account for roughly 30 to 40 percent of total energy consumption. As rack densities grow and sustainability targets tighten, operators face mounting pressure to optimize thermal management. AI workloads intensify this challenge: high-density GPU and AI racks are rendering traditional air cooling insufficient, accelerating adoption of direct-to-chip and immersion cooling solutions, according to market analysts.

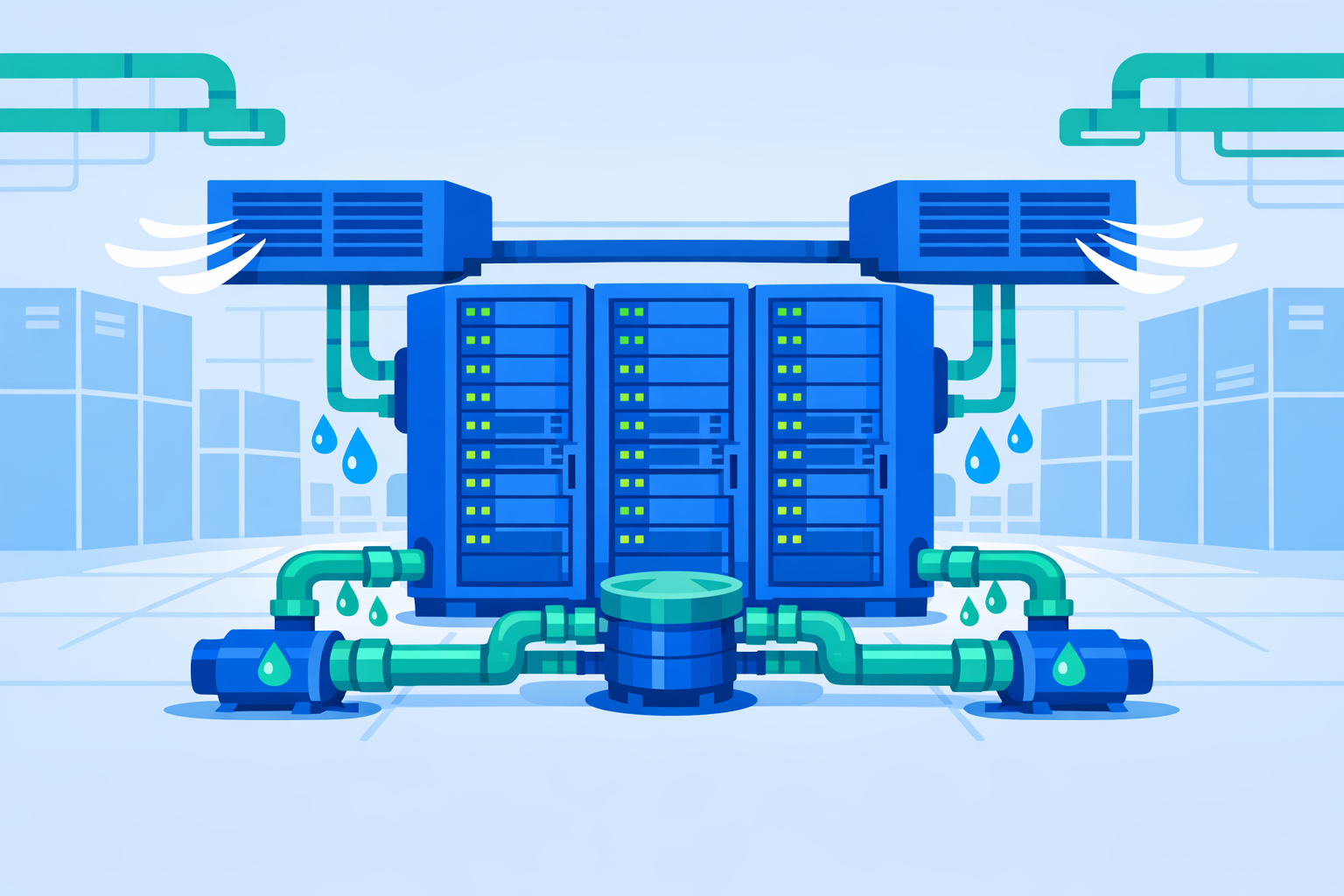

Hybrid architectures-combining conventional CRAC or CRAH air-side units with liquid-side coolant distribution units (CDUs)-have emerged as the preferred transitional model. The assumption that direct liquid cooling eliminates the need for air cooling is a misconception. Even the most advanced liquid-cooled servers contain components not covered by cold plates-memory modules, NVMe SSDs, and voltage regulator modules still depend on proper airflow management. A hybrid design uses liquid to cool high-TDP processors while a secondary air-cooling loop manages the rest of the chassis.

Efficiency data supports the hybrid approach. A joint NVIDIA-Vertiv analysis published by the American Society of Mechanical Engineers found that a 75% liquid / 25% air hybrid configuration reduced facility power consumption by 27% and cut total site energy use by 15.5%, according to Vertiv. Compared to traditional air cooling, liquid systems can deliver up to a 45 percent improvement in power usage effectiveness (PUE), often achieving values below 1.2. Closed-loop designs also drastically reduce water consumption by avoiding the evaporation losses common in air-cooled systems.

On the refrigerant side, hydrofluoroolefins (HFOs) such as R-1234yf and R-1234ze are current front-runners with ultra-low GWP ratings below 10, though they introduce mild flammability risks. HFO/HFC blends such as R-454B and R-513A offer transitional solutions with more familiar handling characteristics. Natural refrigerants including CO₂ and ammonia represent the lowest-GWP options but carry unique design and safety challenges that can make them unsuitable for indoor or hyperscale environments. Chemours' R-454B (Opteon XL41) carries a GWP of 466, representing a reduction of more than 77% versus R-410A, according to ACHR News.

Major OEMs have moved to respond. Schneider Electric launched its first low-GWP-compliant InRow cooling product in April 2026, an 11 kW unit using R-32, with additional models to follow in phased portfolio transitions, according to Schneider Electric. The company stated it redesigned and operated cooling units with low-GWP refrigerants in live data centers starting in 2023 in North America, with additional units deployed in Europe since 2024. Vertiv has likewise been redesigning its product lines to offer low-GWP refrigerant options across its portfolio.

The shift carries infrastructure consequences beyond refrigerant chemistry. Mechanical rooms now require active ventilation, gas detection, and automated isolation logic tied directly into the building management system. Controls platforms must monitor pressure and temperature while actively responding to leak thresholds, triggering safety protocols in real time. Refrigerant mass limits per zone may also constrain system layout-operators may need to segregate cooling systems to reduce charge volume per equipment room or hallway.

Staff readiness is an equally pressing concern. Liquid cooling requires specialized expertise that many organizations currently lack. Maintenance procedures grow more complex, demanding technicians familiar with hydraulic systems rather than traditional HVAC equipment-creating a talent gap and operational pressure during the transition. The introduction of A2L refrigerants and natural alternatives requires updated safety procedures and training across all levels of the HVAC industry. The EPA and organizations including ASHRAE and UL have updated codes to ensure proper installation, servicing, and compliance.

Outlook

The global data center cooling solutions market was valued at USD 11.65 billion in 2025 and is projected to reach USD 30.98 billion by 2034, at a CAGR of 16.2%, according to market analysts. Contractors will need to procure low-GWP-compliant equipment with manufacturing and installation lead times in mind to ensure systems are operational ahead of the January 1, 2027 federal deadline. Facilities planning phased IT load growth should account for the likelihood that successive build-out phases may require different chiller specifications, according to Vertiv-a design complexity that demands early coordination among mechanical engineers, IT planners, and procurement teams.